- Banker's Edge

- Posts

- Stock Buyback Case Study

“Stock buyback, in my opinion, is a very good thing to do when your stock is cheap.” - Jamie Dimon, CEO of JPMorgan Chase & Co.

While public bank stock prices slowly but sporadically rebound from steep declines in March due to the liquidity crisis, publicly traded banks are doubling down on their effort to repurchase stock. Tompkins Financial Corporation (NYSE: TMP), Princeton Bancorp, Inc. (NASDAQ: BPRN), and HarborOne Bancorp, Inc. (NASDAQ: HONE) were among the many who announced on their recent Q2 earnings calls the beginning or continuance of stock buybacks.

To demonstrate the accretive impact of these share repurchases, let's consider a bank that conducted share buybacks in both 2020 and 2021. We'll compare the performance of their shareholders since then with how they would have fared if the bank hadn't opted for stock buybacks.

Background

Citizens Community Bancorp, Inc. (NASDAQGM: CZWI) headquartered in Eau Claire, Wisconsin in the northern region of the Bluff Country of the Midwest, is a bank holding company with approximately $1.7B in assets as of June 30, 2023. Its subsidiary bank, Citizens Community Federal N.A., offers traditional community banking services through 23 locations in the Chippewa Valley Region in Wisconsin as well as several suburban and rural communities in Minnesota.

In October 2019, CZWI announced that it would begin repurchasing its common stock with the board approving repurchases up to 5% of the roughly 11.3 million shares outstanding. At the time, the common stock of the bank holding company was trading slightly above book value.

Thereafter, CZWI’s board of directors opted to issue $15.0 million in subordinated notes in August 2020 for general corporate needs and in part to finance further repurchases that were announced in December of that year. In December 2020, CZWI’s board again approved the company to repurchase up to 5% of its outstanding common shares.

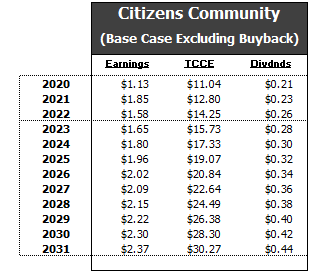

Before we proceed with modeling potential share repurchases, let's establish a baseline by considering the company's financials if it had decided not to engage in share repurchases and had not issued the associated subordinated debt.

These financial projections are for illustration purposes only and were developed by The Bank Advisory Group based on its financial analysis of the company’s historical performance. CZWI provided no input or guidance. Years 2020 – 2022 reflect actual performance modeled to exclude the accretive effects of share repurchases and the assumed debt’s effect on Tangible Common Core Equity.

Some key assumptions are made above that will be repeated in the proceeding analysis:

Asset growth and earnings for years 2020 - 2022 are in line with the actual performance of the bank.

Asset growth and earnings for years 2023 - 2031 are projected in accordance with forecasted interest rates, market conditions, and historical averages of the bank.

A marginal tax rate of 28.90% (21% federal + 7.9% state).

Dividends per share for 2020 - 2022 are in line with reported dividends to shareholders.

Dividends for years 2023 - 2031 are projected in accordance with historical year-over-year increases and remain unchanged between the different scenarios to effectively measure the tangible capital impact of the stock buybacks.

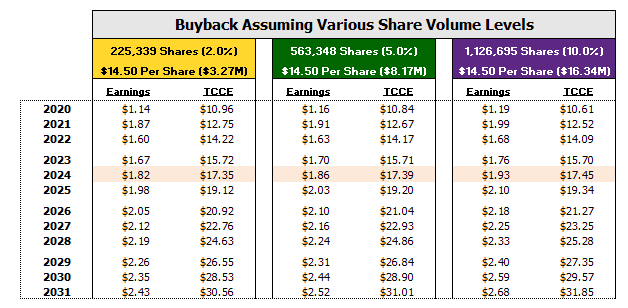

Illustrated below are scenarios outlining the repurchases of 225,339 shares (2.0%), 563,348 shares (5.0%), and 1,126,695 shares (10.0%) at a price of $14.50 per share in 2020. These projections consider the inclusion of corresponding subordinated notes amounting to $3.3 million, $8.2 million, and $16.4 million, respectively. These subordinated notes would follow the same terms and agreements as the subordinated notes CZWI issued during their $15.0 million subordinated debt placement in 2020. We note that per share dividend projections have been removed from the following analysis as they are consistent with the base case projections and would therefore be redundant.

As highlighted above, by year 2024 the financial impact of the larger repurchases of 5.0% and 10.0% have overcome the interest cost of the initial sub debt issuances to be more accretive to tangible equity than the 2.0% level.

Compared to the base case of no repurchases, all three of the share repurchase levels are accretive to tangible equity by 2024 and continue to be increasingly accretive moving forward regardless of the corresponding debt level utilized to fund the repurchases.

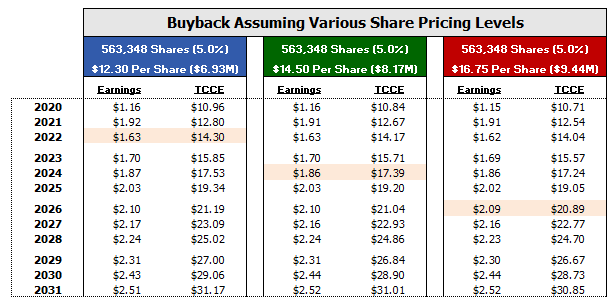

Alternatively, if we assume that CZWI purchases the midpoint number of shares as assumed in the prior scenario (563,348) but we adjust the per share price 15% above and below the $14.50 per share price assumed above, we get the following results.

As illustrated above, at $12.30 per share, it takes CZWI two years to become accretive to tangible equity above the base level. At $16.75/share CWZI is not accretive to tangible equity until 2026.

So Far, So Good

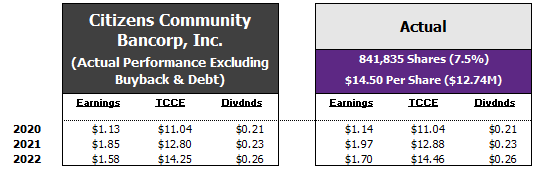

Rather than muck about in the hypothetical, let’s look at our base case vs. what the bank holding company has actually reported through year-end 2022.

Despite our model projecting a four-year break-even on tangible equity, CZWI was able to accrete more tangible equity in all three years from 2020 — 2022 and breaking even from the very first year of the buybacks.

Conclusion: Risk vs. Reward

Despite the rosy returns in the above case, buybacks are certainly not without their risks:

Financial Risk: Can you reasonably achieve the level of projected earnings without the equity that is returned to shareholders? Is there a better use of capital/borrowing capacity?

Operational Risk: Do you have the controls in place to carry out the transaction?

Cultural Risk: How do non-insider shareholders feel about your stock? Do they have a perceived need for liquidity? (It is our observation that community banking directors often substitute their personal perspective on holding shares of the bank when considering this question. But such attitudes are centered on the directors’ personal involvement in the bank and the communities it serves. However, many smaller shareholders have no such connection and feeling for the bank, having worked and lived far away from the bank’s market area for some time if not for the entirety of their lives.)

While the performance on a per share basis above speaks for itself, it’s worth reiterating the power of buying back shares:

Eliminating outstanding shares appreciates earnings per share for remaining shareholders.

Eliminating outstanding shares can provide liquidity to shareholders who desire liquidity and who do not have an active relationship with the bank.

Earnings per share appreciation produces ongoing appreciation in tangible equity capital.

As mentioned in our previous newsletter, some of our clients are seeing declines in their valuations year-over-year due to the rising cost of capital and falling public bank stock pricing. Correspondingly, a growing number of our clients are executing formal tender offers for shares of their outstanding common stock, and the response by smaller shareholders (and sometimes larger shareholders!) is almost always well in excess of their initial expectations.

Reflecting on the scenario where CZWI repurchases their shares for 15% less than the midpoint, the accretion to tangible common core equity was projected to only take two years. While declines in share price certainly aren’t celebrated among board rooms, they should at the very least awaken the key stakeholders of the bank to the possibility of repurchasing shares at relatively lower valuations. After all, Jamie Dimon would and he’s a pretty good allocator of capital.