- Banker's Edge

- Posts

- June 2023 Valuation Update

June Valuation Update

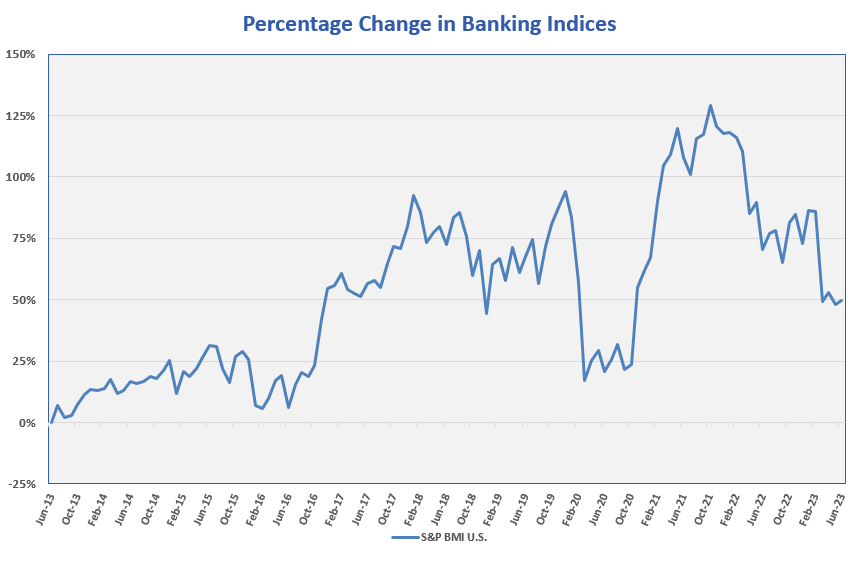

Despite a temporary decline in the risk-free rate during March and early April, the 20-year U.S. Treasury is now back above 4% and was 4.06% as of June 30, 2023. Correspondingly, the equity risk premium at June 30, 2023 has reached levels not seen since 2008-2009. This produces negative effects on the discounting of future cash flows. The good news is that bank earnings are up for many banks, which partially mitigates the higher discount rates. However, bank valuations for our community bank valuation clients have been negatively affected by the decline in public bank stock pricing during 2023. As illustrated in the following chart showing the U.S. Broad Market Bank Index, public bank stock pricing took a fall in March 2023, similar but not equal in magnitude to the decline seen in March 2020. Public bank stock pricing has seemed to reach a bottom since the liquidity crunch of this Spring but will continue to place downward pressure on valuations as it nears levels not seen since 2020.

For our community bank valuation clients with rising earnings over the last twelve months and a rate insensitive deposit base going forward, we expect that their mid-year 2023 valuations will be flat to slightly down due to the effect of public bank stock pricing on the Market Value Methodology. For banks with weaker earnings over the last twelve months and/or a rate-sensitive deposit base moving forward, mid-year 2023 valuations will be down due to the increase in the discount rate on a weakened earnings outlook in the near-term, together with the effect of public bank stock pricing on the Market Value Methodology.

Deposits: 2024 is the New 2019

While banks were flush with liquidity following the onset of COVID-19 and the subsequent fiscal stimulus, they didn’t worry much about growing deposits because most had more than they needed. However, the battle for stable funding was rekindled in 2022 once stimulus money began to drain out of the system while at the same time rising interest rates increased deposit pricing competition. Whether the U.S. goes into the long-expected recession or not, the general consensus around the Fed’s direction draws some similarities to what we saw in 2019 with an uncertain economy and projected rate cuts. It would do banks well to revisit what those rate cuts meant for banks at that time to form a strategy for what might lie ahead.

Let’s think back, as daunting as it may seem, to a pre-COVID world. The year is 2019. The Fed had been steadily making progress in their quantitative tightening plan through small (microscopic compared to what we saw in 2022) and consistent rate hikes in the growth cycle following the Great Financial Crisis of 2008 and 2009. As the economy started to show signs of cracking in late 2019, the Fed reversed course with the fed funds rate ending the year at 1.55% compared to 2.40% in January 2019. The Fed’s reaction was consistent with its historical inclination to cut rates more quickly than it raises rates.

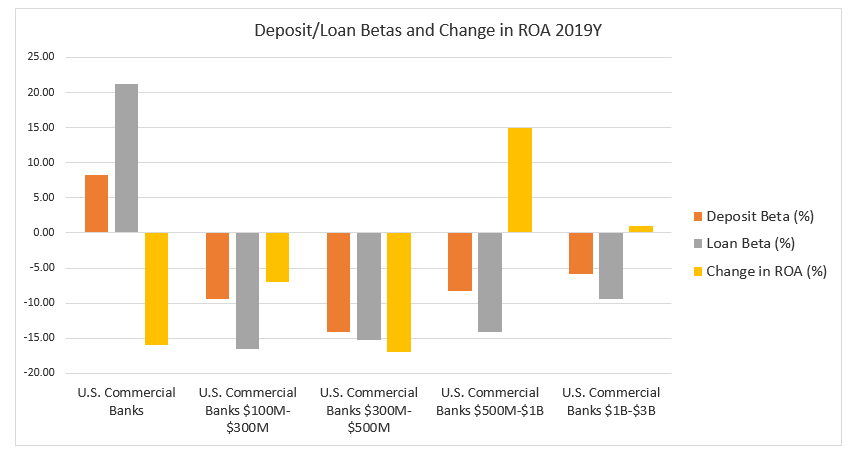

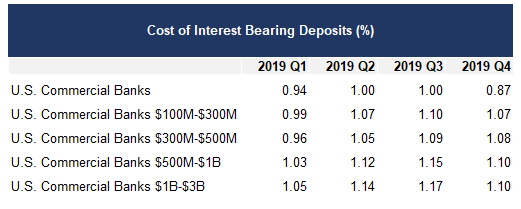

Another relic from the 2019 time capsule: the deposit beta. Perhaps you vaguely remember the term before it got cast to the wayside in favor of the grossly overused phrases “these unprecedented times” or “new normal.” As a refresher, the deposit beta is the portion of a change in the fed funds rate that banks pass on to their deposit customers. A beta of 100% suggests a bank that will pass on all of a fed funds rate increase/decrease to their depositors. As illustrated in the chart below by the negative beta (deposit rates moving opposite of fed funds), banks below $3 billion in assets ended the year with an overall increase in the cost of interest-bearing deposits despite the rate cuts that began in August 2019.

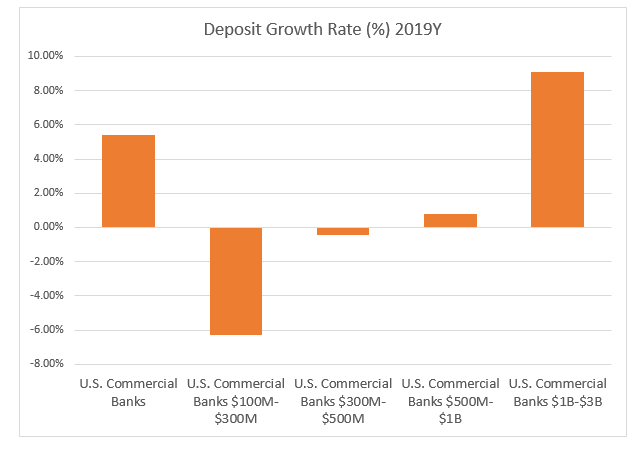

Moving from U.S. commercial banks with $100M-$300M in assets to U.S. commercial banks with $1B-$3B in assets, deposit growth increases and deposit betas increase (except for the $300M-$500M group that raised deposit rates the most during 2019).

The larger the bank, the more quickly it responds to changes in interest rates on both loans and deposits. It’s worth noting that the larger banks in this group were already paying more than their smaller peers beginning in 2019, then they came down to a rate level that was just slightly elevated by year-end. However, despite how a bank chooses to respond to monetary policy, we believe that there’s a better, more proven way to preserve the net interest spread.

A Better Way

Contrary to popular belief, banks historically perform better in a declining interest rate environment. It’s a natural consequence of lending long and borrowing short. Even better off are banks that simply do not play the rate game with their depositors from the start.

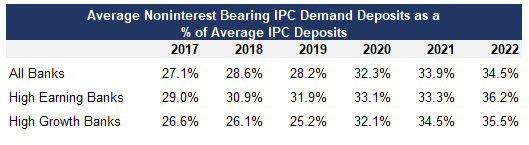

Data Source: The Profit Improvement Report Survey, produced annually by The Bank CEO Network.

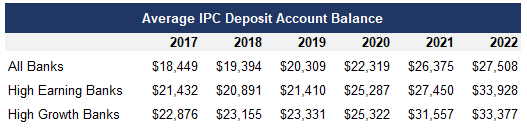

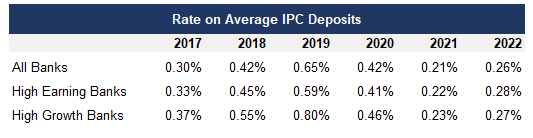

As illustrated in the preceding table from data collected through The Bank CEO Network, high earning banks consistently (except for 2021) reported a greater percentage of average noninterest bearing Individual & Partnerships, and Corporations (IPC) demand deposits as a percentage of average IPC deposits than their lower earning peers. Or, put another way, banks that have less reliance on interest-bearing core funding typically perform better than those banks that have more regardless of what they pay for interest-bearing deposits. Additionally, the high performing banks also reported the highest average deposits per IPC account (i.e., high performing banks have deposit accounts with larger average balances). Interestingly, the highest performing banks paid slightly higher rates than average on their core funding during rising interest rate environments (2017, 2018, 2022). However, they were able to respond to falling rates, like what we saw in 2019, much quicker than average, reporting a rate on average IPC deposits six basis points below all banks.

Data Source: The Profit Improvement Report Survey, produced annually by The Bank CEO Network.

Data Source: The Profit Improvement Report Survey, produced annually by The Bank CEO Network.

The trend should now be evident — good bankers cut deposit rates quickly when interest rates are falling because they have stable noninterest bearing funding on which to rely. The best performing banks are proficient at securing both sides of their commercial lending relationships. As we look ahead to, most likely, two more rate hikes this year and then rate cuts beginning sometime next year, it’s imperative for banks to look closely at the funding side of their balance sheets in order to determine how they’ll fare in a different rate environment.

What if your bank doesn’t currently have a lot of large corporate depositors? Have your lenders actively and aggressively pursued the loan relationships for deposits? Many lenders have forgotten during the last couple of years to solicit noninterest-bearing “corresponding” deposits because, frankly, their bank was flush with cheap funding. Now is the time to coach your lending staff on “getting” the other side of the lending relationship. When rates fall, these stable funds will be key to improving the bank’s deposit beta thus enhancing a bank’s ability to lower rates in its interest-bearing deposit base. Additionally, securing both sides of a customer relationship deepens the bonds of those relationships to your institution.

For a more creative approach, you could use the publicly available PPP loan data to determine which businesses in your market(s) used a large national/regional bank to facilitate their PPP loan. Then, direct your lenders to ascertain if those borrowers have their deposits there as well.

Finally, some community banks have successfully utilized banking-as-a-service and other fintech platforms to boost their deposit bases while sharing in interchange income with the fintech acting as the intermediary. Community banks are uniquely positioned to offer this thanks to the Durbin amendment which allows them to charge higher interchange fees than banks larger than $10 billion.

Regardless of the monetary environment in which we find ourselves and the strategy you employ, there appears to be a recipe for success that high performers follow: secure large noninterest-bearing deposit accounts or risk not being able to improve your net interest spread in a declining interest rate environment.