- Banker's Edge

- Posts

- Year-End 2023 Valuation Update

Year-End 2023 Valuation Update

Publicly-Traded Banks Rally While Discount Rates Fall

Brandon McCown

January 18, 2024

At the Bank Advisory Group, January marks a season of transition, as it does for most folks. The turning of a new calendar year marks a transition for BAG into a busy season of end-of-year valuations. And if bank valuation practitioners were polled in September 2023 on their expectations for end-of-year valuations, most would’ve shuddered to provide an answer.

However, with the forward outlook provided by the Federal Reserve at their December meeting, many of the assumptions that were being projected onto end-of-year valuations have changed for the better. Jerome Powell may not have been climbing down bankers’ chimneys, but he had no shortage of gifts to deliver to bank investors this past December.

Publicly-Traded Bank Stocks

When valuing a minority ownership position in a privately held community bank, the Bank Advisory Group employs a combination of a Market Value Approach and an Income Value Approach. The Market Value Approach seeks to find banking institutions with publicly-traded stock that are reasonably comparable to the subject bank (based on financial metrics such as tangible equity and return on assets) to determine appropriate pricing indicators for the subject banking franchise.

Throughout 2023, we witnessed the Market Value Approach consistently compress values for community banks as the public bank market faltered following the March 2023 “Liquidity Crisis.” However, publicly-traded banks, like almost all publicly-traded equities, experienced the famed “Santa Claus Rally” following the Federal Reserve’s announcement to continue their rate hike pause through the end of the year while the FOMC penciled in an additional and unexpected rate cut in their 2024 “dot plot” (a forecast of officials’ expectations of the federal funds rate).

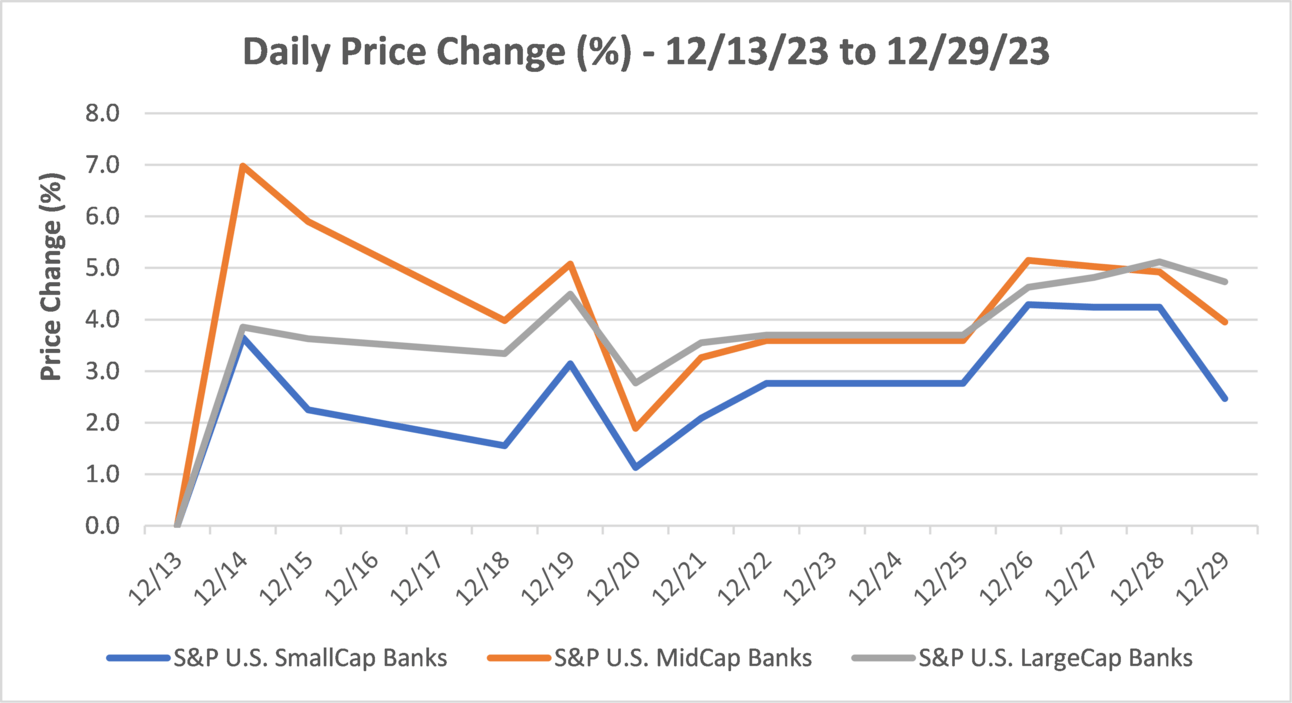

The chart below shows the bank index price movements of publicly-traded banks categorized by market capitalization in the 12 trading days following the Federal Reserve’s press conference on December 13, 2023:

As illustrated in the chart above, publicly-traded bank stocks experienced a dramatic price increase immediately following the previously mentioned Federal Reserve announcement on December 13th . The S&P U.S. MidCap bank index had the largest increase, likely the result of regional banks experiencing the largest decline earlier in the year (as shown below) due to most of the bank failures occurring in this segment.

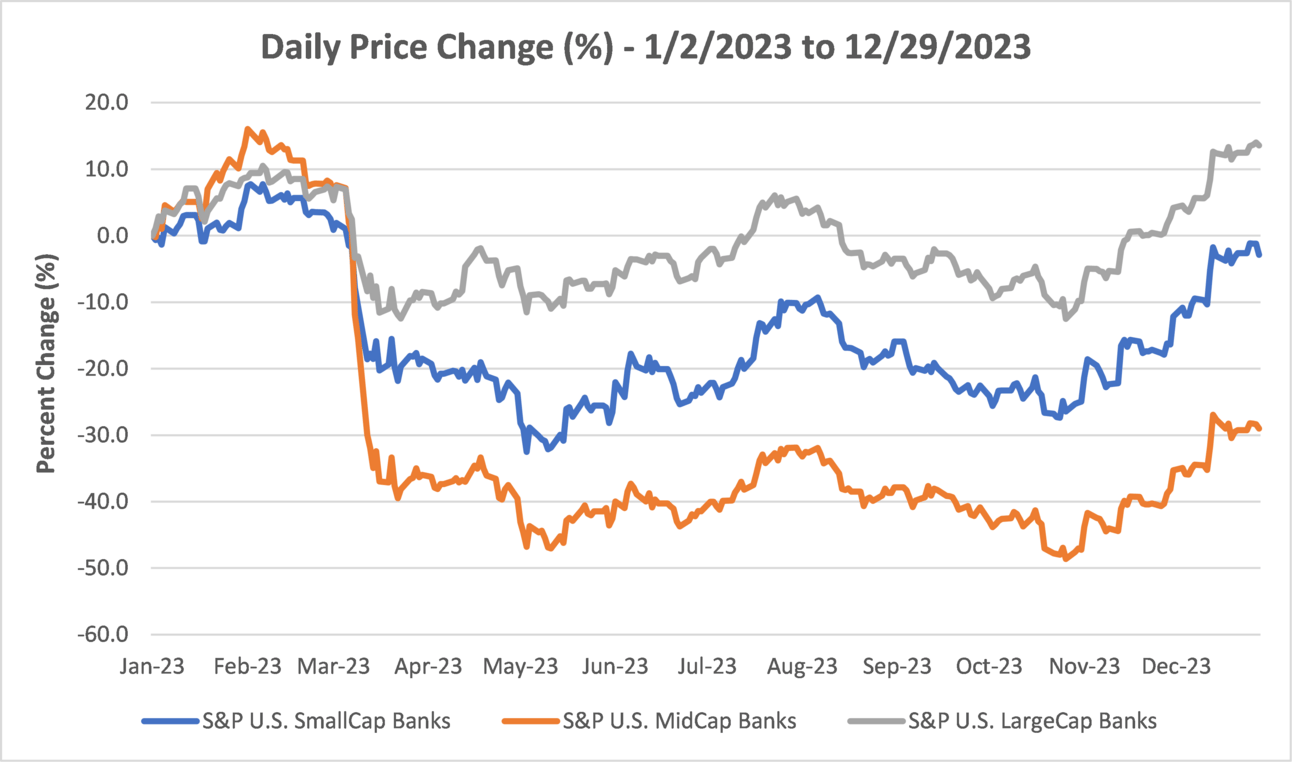

As illustrated above, bank stock prices appeared to have bottomed in May 2023 for U.S. SmallCap banks, while U.S. LargeCap and MidCap banks saw low points in November 2023 that were similar to what they had experienced earlier in the year. LargeCap bank stocks were the only segment of the market to post a positive YTD return for 2023, with SmallCap roughly breaking even and MidCaps ending approximately 30% down from the beginning of the year.

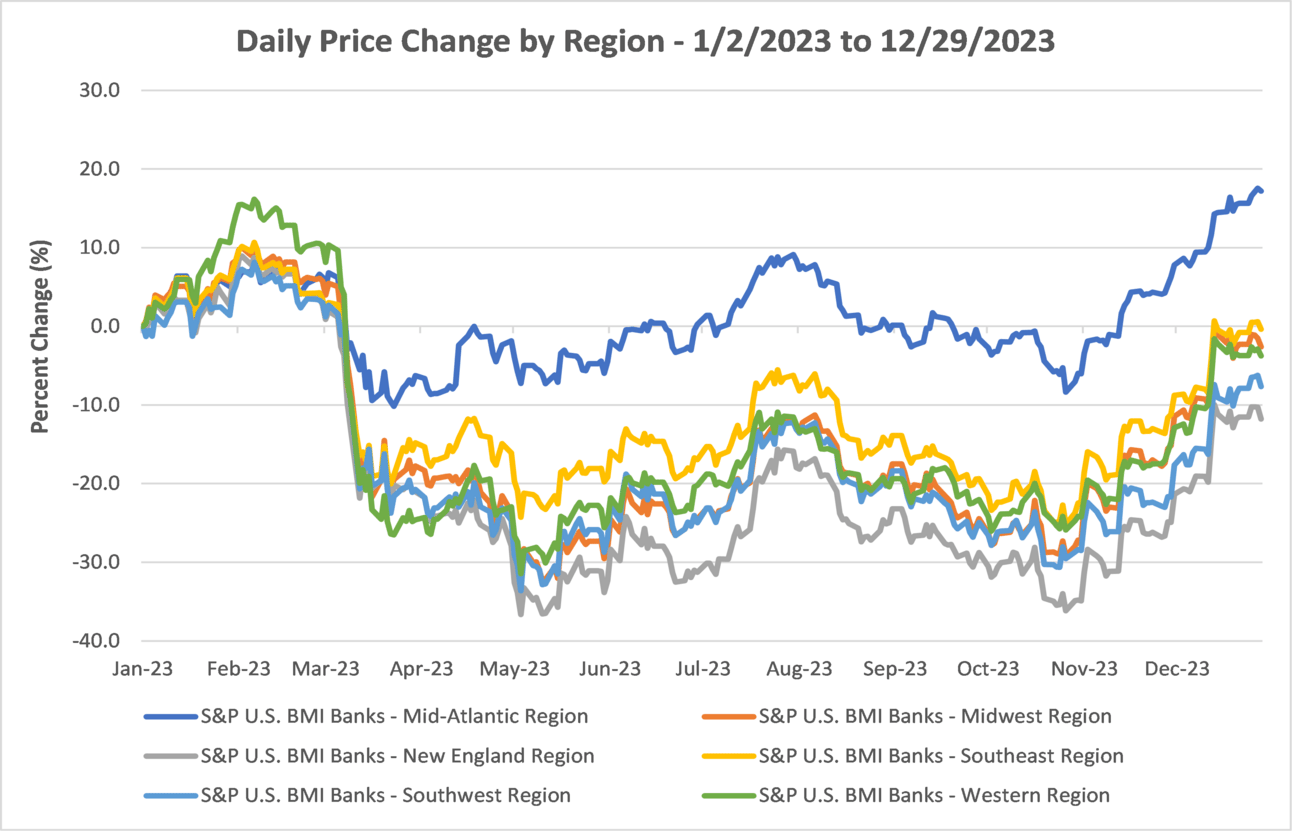

While national bank pricing is a good barometer for the overall publicly-traded bank market, our philosophy at the Bank Advisory Group, when applying the Market Value Approach, is to lean more heavily (when permissible) on regional bank pricing for the region in which the subject bank operates. So, looking at bank stocks on a regional basis, the S&P U.S. Broad Market Index (“BMI”) – Mid-Atlantic Region was the only index to post a positive YTD return for 2023. Publicly-traded banks in the S&P U.S. BMI Southeast finished the year approximately where they started while publicly traded banks in the S&P U.S. BMI Midwest, West, Southwest and New England posted varying degrees of negative YTD returns for 2023.

From a valuation perspective here at the Bank Advisory Group, the December rally in bank stock prices will help to buoy year-end values from the trough of mid-year 2023. However, in our conversations with clients over the past several months, many community banks have 2024 earnings outlooks that are flat to down from 2023. This reality will, in some cases, offset the increasing Market Value Approach.

Bank Earnings Forecasts

In conjunction with the Market Value Approach, the Bank Advisory Group also employs an Income Value Approach. The Income Value Approach is a 12-year look forward of projected financials for the bank. The bank’s net earnings for the 12-year period are then discounted back to the valuation date to determine a present value of future earnings. As with any present value calculation, the near-term projections have a greater impact on the overall present value conclusion.

As noted, most bank management teams are projecting earnings to be flat to down in 2024. While rate cuts, should they occur, will help to ease banks’ cost of funds, it’s not clear how much impact can be expected on earnings this year. And while many bankers continue to see strong but moderating loan demand in their respective markets, many don’t have the needed liquidity to pursue the loan relationships. Consequently, many banks anticipate minimal loan growth.

Again, the projected rate cuts should ease the burden on liquidity and capital as underwater investment securities portfolios come up for air, so to speak. However, how much impact can be expected on earnings this year is unclear and most bankers are choosing to be cautious in how they approach their forecast.

One thing that is for certain, however, is the reality that S corp. banks are another year closer to losing the Qualified Business Income Deduction that was part of the 2017 JOBS Act, set to sunset in 2025. Without knowing the results of November’s election, and the unlikelihood that either party would have enough time to renew the policy (given that it isn’t a topic of discussion currently) means that bank shareholders can expect this deduction to disappear come 2026.

Management teams should begin considering whether remaining as an S Corporation is prudent for its shareholders as the tax burden, and thus the dividends required to be distributed to shareholders, increase. From a bank stock valuation perspective, this will have a greater negative impact on the Income Value Approach than it did in 2022 given that the projected year for the tax deduction ceasing is one year closer (resulting in lower earnings outlooks in the near-term).

Discount Rates

While earnings outlooks may not be as optimistic as they were a year ago given the much higher funding costs that bankers are navigating, the good news is that the risk-free rate fell in December in connection with the increased expectation of rate cuts in 2024. This is important because to discount future earnings back to their present value, the valuation analyst must determine an appropriate discount rate to apply. While our philosophy at the Bank Advisory Group is to employ several different methodologies when determining the appropriate discount rate; regardless of which methodology you use, it all begins with what return an investor could reasonably expect from a risk-free investment (the 20-year U.S. treasury yield in our case).

As of December 29, 2023 (the last trading day of the year), the risk-free rate had fallen to 4.20%, down from 4.92% as of September 30, 2023 and up slightly from the 4.14% reported at December 31, 2022. During December 2023, the expected return on a market portfolio also declined to a similar level as year-end 2022. The slightly higher risk-free rate as compared to a year ago but similar expected return on a market portfolio means that we can expect that discount rates should be similar to where they were at year-end 2022, all else being equal.

Along with the Santa Claus Rally, discount rates falling from their recent highs will serve as a buoy to year-end values as it will prevent future earnings from being as deeply discounted as they had been earlier in 2023.

Conclusion

All valuations are highly individualized as each subject bank poses unique risks and advantages so it makes it difficult to say with certainty where year-end valuations will be across the board relative to where they were a year ago. However, we anticipate the different push and pull factors previously discussed in this newsletter to affect banks to varying degrees.

We can say that along with bank shareholders, we’re thankful for the end-of-year rally in bank stocks and the corresponding decline in the risk-free rate that will help to support valuations from declining too much until a more favorable macro-environment returns.