- Banker's Edge

- Posts

- Thoughts on End of Year Valuations and State of the Market Update

Thoughts on End of Year Valuations and State of the Market Update

Brandon McCown

January 30, 2025

2024 Banking Highlights

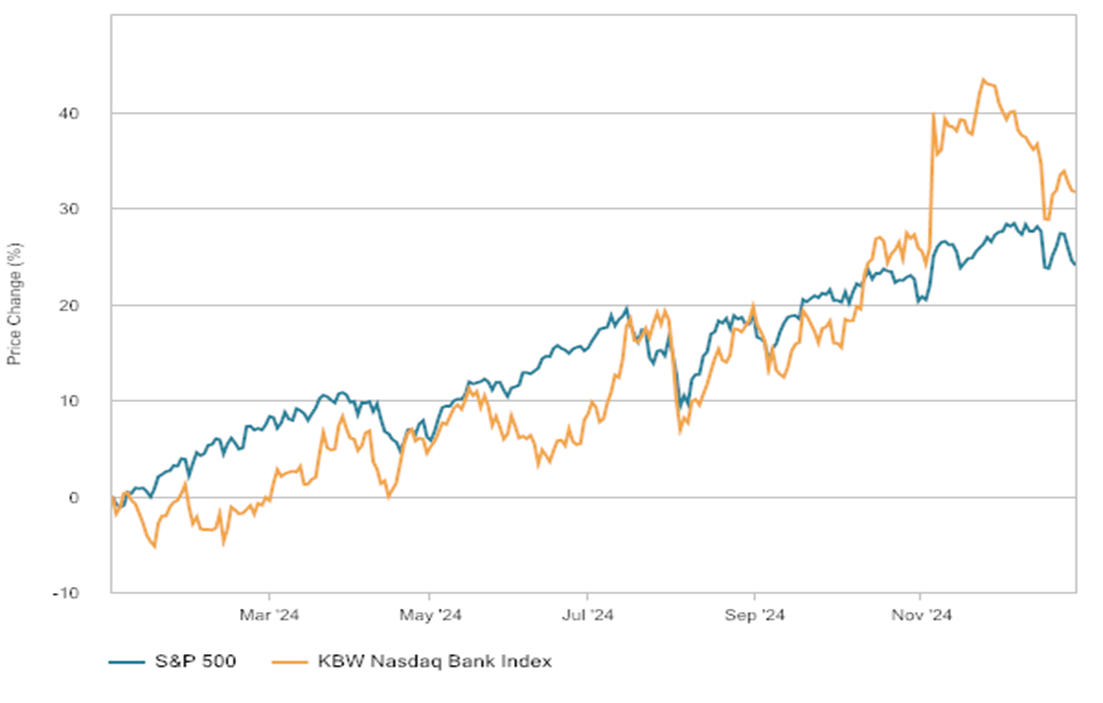

2024 turned out to be the near opposite of what most were prognosticating for banks a year earlier. While many anticipated the year would be marked by the Fed missing its soft-landing target and spinning the economy into a mild recession, the broad market roared and, surprisingly, publicly traded banks beat the market index as illustrated by the 31.65% 2024 return of the KBW Nasdaq Bank Index compared to the 24.01% return for the S&P 500 during 2024.

Since the 100-basis point rate decline during the last four months of 2024, the Federal Reserve’s latest guidance indicates that they’re in a hold pattern until more information is available on inflation and the labor market. Whether the Fed can achieve its desired 2.0% inflation target is up for debate. But for now, it seems (in keeping with its dual mandate) the central bank has successfully avoided the worst-case scenarios of hyperinflation and/or a recession while fostering a strong labor market. The recent rate cuts have, for many of our clients, provided a welcome reprieve to their cost of funds.

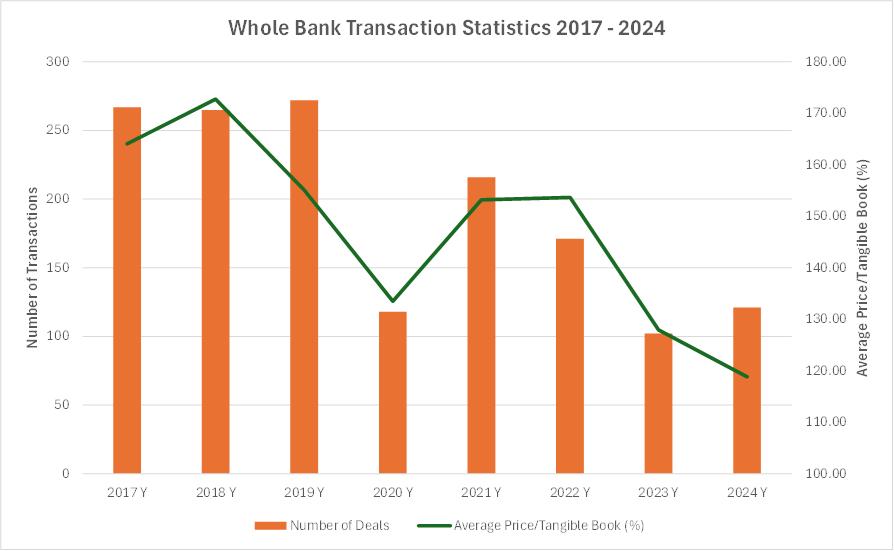

Despite the rally in publicly-traded bank stock prices during the second half of the year and the normalization of the yield curve, whole-bank acquisitions remained sparse in 2024. Many banks are still hamstrung by large unrealized losses in their bond portfolios and loan marks on their loan portfolios that are making deals difficult to complete. Prices paid for whole banks are reflective of this low demand market dynamic. As we’ve told many a client over the past 18 months, now is not the time to be selling your bank.

Year End Stock Values

The combination of the bank stock market rally and more optimistic near-term earnings outlooks as rates decline and deposit pricing pressure normalizes leads us to believe that many year-end values will be up from a year ago.

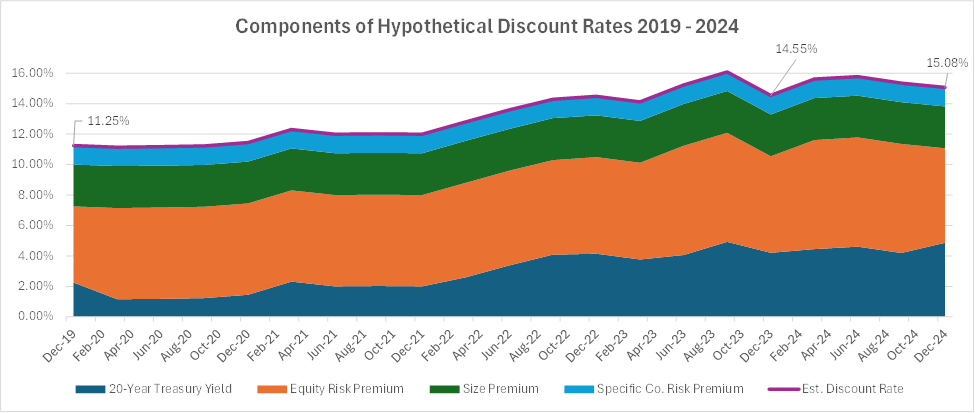

There will be exceptions, particularly for low performers and potentially for highly-asset sensitive banks that stand to see earnings decline as rates fall. Banks with lower near-term earnings will face further downward pressure on their stock value as discount rates remained slightly above year-end 2023 figures throughout 2024, as illustrated in the following chart. Furthermore, at year-end 2024 the discount rates were higher than year-end 2023 due to the recent rise in the 20-year treasury. Better near-term earnings outlooks combined with a higher discount rate could create a “wash,” leaving the present value of future earnings flat from a year ago. In this case, much of the direction of the value would hinge on last twelve months performance compared to the subject bank’s publicly-traded peer group at the end of 2024 and where the comparative guideline group was trading at that time.

BAG Internal Data

Trends to Watch Entering 2025

A new administration in the Oval Office will certainly be a driving force behind emerging trends this year. Tax law changes, and particularly whether the Trump Administration can persuade Congress to extend the 2017 JOBS act, will be important for banks - especially those that operate as S-corporations today due to the 20% qualified business income deduction that will sunset at the end of 2025 if this provision of the JOBS act is not extended. If the 20% exclusion is not extended, then there will likely be a flurry of conversions from S to C corporations.

As has been the case for the last two years, plenty of focus will be on Jerome Powell and the remarks and signals coming out of the Federal Reserve. The recent comments from Jerome Powell’s press conferences insinuate that the hard and fast rate cutting cycles that were customary in the past will not be realized unless some external catalyst necessitates it. Instead, the Fed’s most recent remarks suggest that their focus has yet again shifted from concern over the labor market to fears of reigniting inflation. Indeed, futures trading according to the CME Fedwatch tool implies only 25-50 basis points of cuts occurring during the second half of 2025.

CME Fedwatch tool provided by CME Group. www.cmegroup.com.

As banks get cheaper sources of funding to replace higher cost CDs, expect to see an unwinding of the brokered deposits and external borrowings that many banks have relied upon over the last 23 months following the March 2023 Liquidity Crisis. Correspondingly, growth will remain low-to-moderate as many banks focus on recalibrating their balance sheet while waiting to see what the new administration can accomplish.

Delinquencies and charge-offs will likely return to pre-COVID levels. The bogeyman of non owner-occupied CRE in metropolitan areas is a real concern, but most community banks have minimal exposure to that type of credit. Instead, the emerging trend following a few years of historically low asset quality issues is a return to pre-COVID levels of problem assets and charge-offs.