- Banker's Edge

- Posts

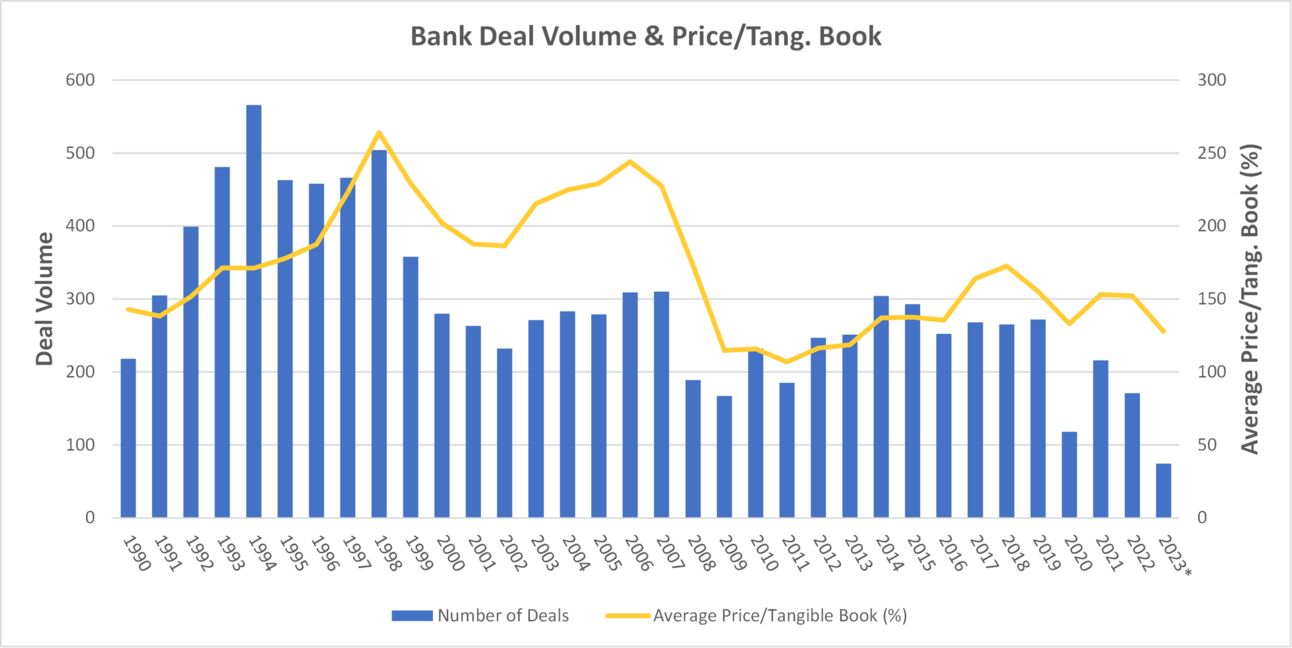

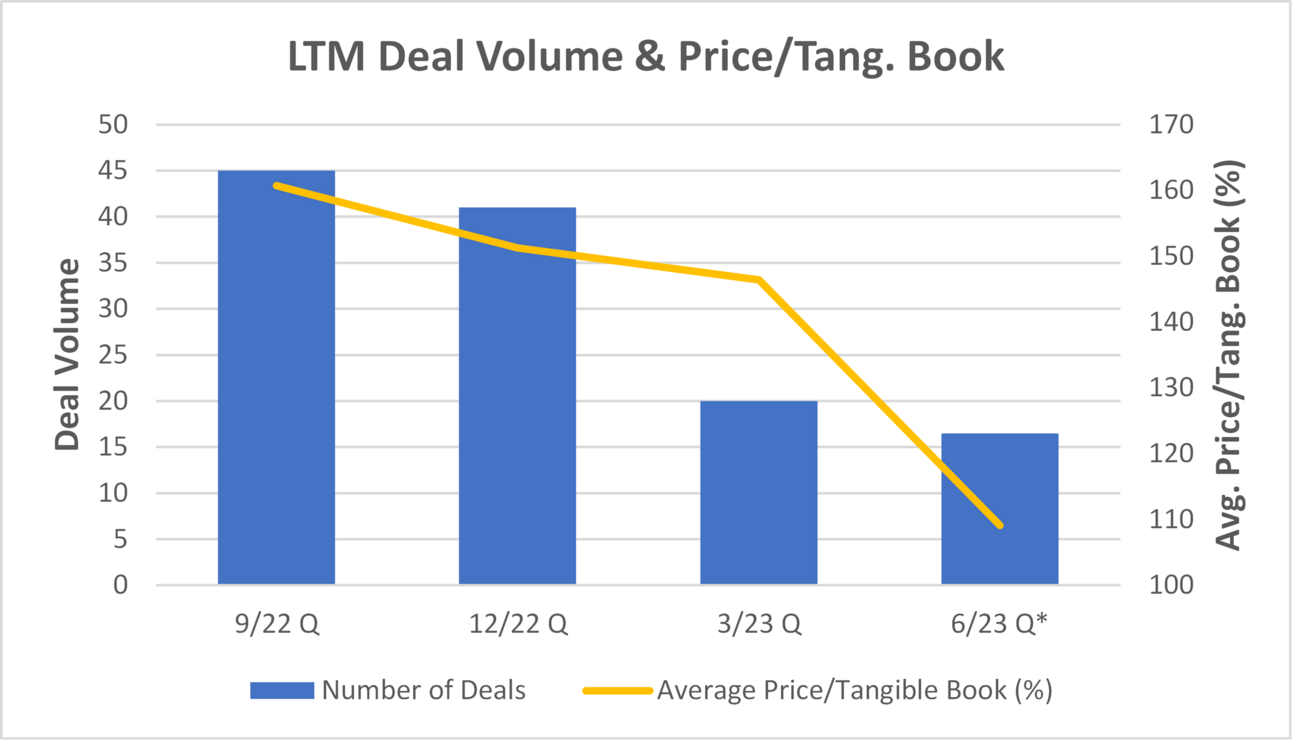

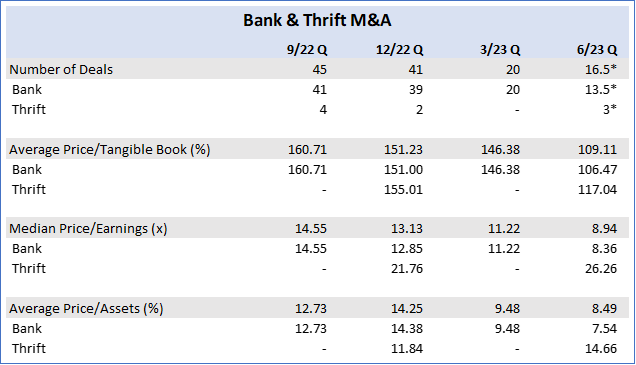

- State of M&A in June

*Deal volume annualized

M&A deal volume is decidedly lower through the first five months of 2023. Economic uncertainty, elevated costs of capital, and, perhaps most importantly, high levels of unrealized losses in banks’ securities portfolios are leading to the slowest transaction environment that we’ve seen in over 30 years (disregarding mid-2020 due to Pandemic effects). Is this justified and how long will it remain like this?

Zooming out from our current landscape as far back as our data will allow (1990), we find that despite the flurry of fiscal stimulus and subsequent economic activity in 2020 and 2021, whole bank transactions never quite recovered to their pre-Covid form on a deal volume basis. The last three years more closely resembled Great Recession era deal activity despite a lack of credit deterioration that was prevalent during the financial crisis. While multiples partially recovered from 2020 declines, albeit supported by quantitative easing, 2023 has brought a steep decline in whole-bank pricing in relation to tangible book value. The average 2023 price/tangible book multiple of 1.28x is 26% lower than the recent 2018 peak of 1.73x. Maybe more telling is that the 1.09x price/tangible book multiple for the second quarter of 2023 is only about 2% higher than the 1.07x price/tangible book that was observed in 2011 following the 2008 downturn.

*Deal volume through 5/31/23 projected to end of quarter

Barring a significant deterioration in credit quality, it appears that the market is currently pricing banks at a discount to normative pricing. However, we wouldn’t expect this current mispricing to resolve in the near future. Significant headwinds persist aided by the recent liquidity crunch which has soured sentiment in the banking industry. All while, the looming question mark of commercial real estate valuations remains. That being said, this market would behoove those well-capitalized banks to take a look at their surroundings for opportunities to bolster their market presence while multiples remain suppressed.

Moving forward we expect M&A activity in banking to remain minimal in the near-term. In the mid-term (late 2024 and beyond) we suspect there will be moderate recovery brought on by tailwinds of slightly lower rates and improved public bank stock pricing. The reactionary regulatory environment in light of the recent liquidity crisis coupled with changes in the technological landscape (artificial intelligence, cyber security, etc.) could also create operational advantages to mergers-of-equals.

*Deal volume through 5/31/23 projected to end of quarter

Why This Banking Crisis is Different

Patrick McKenzie wrote an essay arguing why this may not be the end of the banking crisis but also why that doesn’t necessarily mean financial contagion as it has in the past.

The Banking Crisis Visualized

Figure A3 (pg. 31) from the paper by Jiang et al. (2023) highlights the distribution shift of the equity/asset ratio for 4,800 banks in the United States. As illustrated in this technical paper, the entire distribution shifts left from 2022Q1 to the present based on the authors’ estimate of marking the banks’ assets to market (primarily the securities portfolios). The authors maintain that this movement alone, while alarming given the amount of banks that would be considered insolvent today if their portfolios were marked to market, is not a predictor of bank failure. Rather, the coupling of negative equity and high levels of uninsured deposits are the recipe for a potential bank run which can be seen in Figure A2 (pg. 30) also from the paper by Jiang et al. (2023) plotting the insolvent banks from Figure A3. The size (and color) of the dots correspond with asset size of the bank.

What We’re Seeing

The rise in unrealized losses on securities and the resulting diminishment of stated equity for banks small and large has significantly depressed bank M&A activity as noted elsewhere in this newsletter. Potential sellers are, understandably, hesitant to sell until interest rates decline and/or securities mature and unrealized losses diminish.

Buyers insistent on focusing on stated equity (inclusive of unrealized losses on AFS securities) and applying a price-to-equity multiple consistent with historical averages have sidelined themselves for all intents and purposes. Instead of that approach, The Bank Advisory Group has observed several bank buyers willing to pay total consideration not too dissimilar from what the buyer would have paid prior to the recent uptick in interest rates (provided that the seller’s securities portfolio consists predominantly of securities the buyer is willing to retain post-closing). This results in a sharply higher price-to-stated equity multiple relative to historical averages and produces a higher level of purchase premium as the seller’s securities are “marked to market” in accordance with purchase accounting. As the securities mature post-closing, the “marks” are diminished as the discount is accreted into the buyer’s income, offsetting the initially higher level of goodwill recorded in connection with the acquisition.