- Banker's Edge

- Posts

- Lending in a Late Cycle Economy

Lending in a Late Cycle Economy

Are Banks Being Rewarded for the Risk?

Brandon McCown

November 16, 2023

Bankers took a deep breath toward the end of the third quarter as the pressure on deposit pricing began to subside. And good timing too, because regulators with the Federal Housing Finance Agency stated last week that they would begin unwinding the FHLB from its status as a short-term liquidity source for banks in an effort to return the agency to its original purpose, facilitating mortgage lending. Barring catalysts like the Fed drastically increasing the fed funds rates or any additional failures of large banks, it seems that the rising pressure on deposit pricing and, therefore, net interest margin compression may have run its course for now.

However, while the battle for deposits may be nearing its end, all is not quiet on the banking front. The Federal Reserve released its Senior Loan Officer Survey for October which, to the surprise of no one in banking, reaffirmed the previous surveys’ responses that banks were tightening their lending standards across credit categories. Banks are tightening lending standards while demand for loans is beginning to weaken given the current cost of capital.

As we’ve been told by Jerome Powell and the rest of the governors of the Fed throughout the rate hiking cycle, the measures that the Fed is taking to cool inflation have a lagged effect on the economy. We may be just around the corner from experiencing the lagged effects.

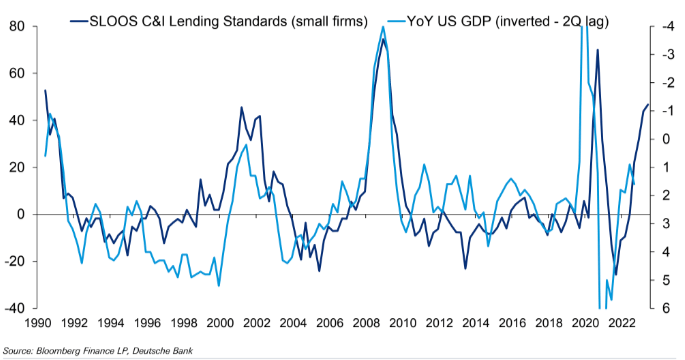

Lending Standards Tighten as Unemployment Creeps Up

Whenever lenders start to report a tightening of lending standards, there’s about a two-quarter lag before GDP begins to decline. Looking at the chart below, the left axis represents commercial & industrial lending standards for small firms as reported by the Senior Loan Officer Survey dating back to 1990 (purple-colored line) with positive numbers representing higher lending standards. The right axis represents the year-over-year US GDP growth (blue-colored line) lagged by two quarters from the associated lending survey results. The YoY GDP growth is inverted to show the correlation that as lending standards increase, YoY GDP growth begins to decline.

This relationship makes intuitive sense. As credit becomes less accessible, companies begin delaying or slashing projects, expansions, etc. In short, the result is a trickle down of lower output. This is not doom-and-gloom speculation, but rather the realization of what the Fed has been aiming to achieve since inflation spiked in 2022.

In the chart, however, there is positive GDP growth for the last two quarters (again, GDP line is inverted) despite the increase in lending standards. We would not expect this to continue given the previous 30 years of data showing the opposite correlation.

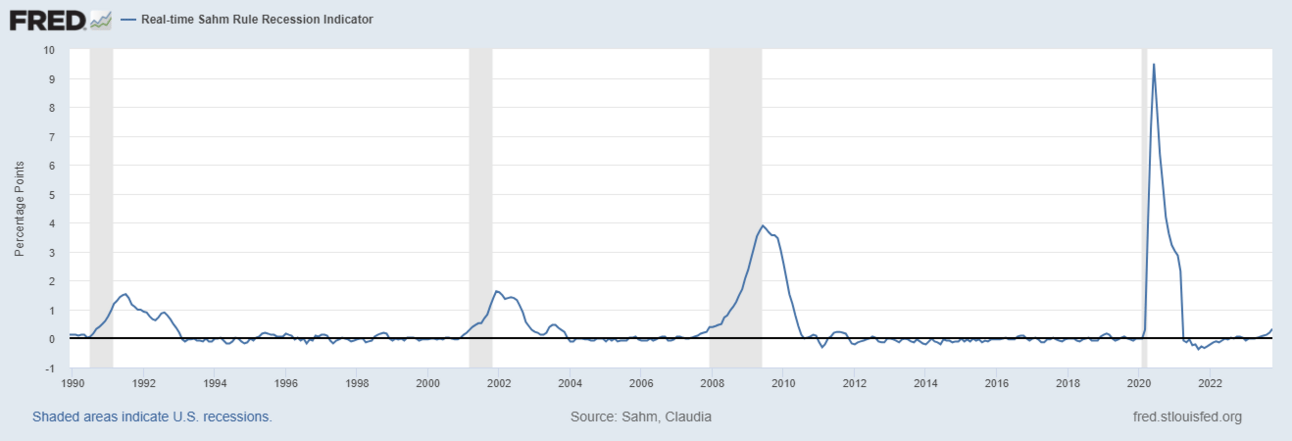

Further, recent reports show that the job market is more fragile than earlier in the year, likely the reason the Fed elected at its November meeting to pause rate hikes. The chart below illustrates the Sahm rule dating back to 1989 with the blue line illustrating the unemployment rate and the shaded areas noting recessionary periods. The Sahm rule dictates that when the three-month moving average of the unemployment rate rises by 50 basis points or more relative to its low during the previous twelve months, then the economy is in the beginning of a recession.

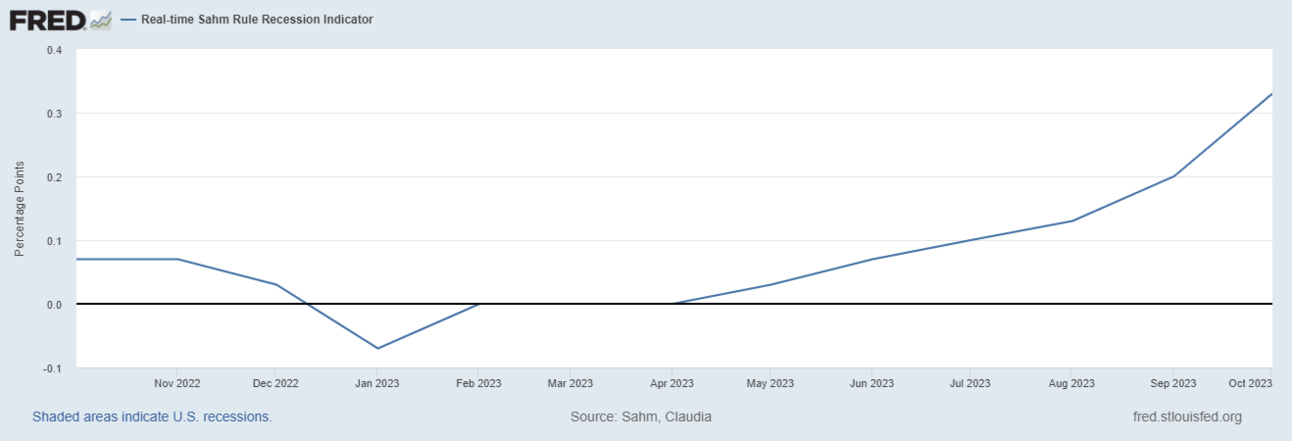

The following chart zooms in on the last twelve months of data.

As of October 2023, the three-month moving average for the unemployment rate was 4.3%. The low of the three-month moving average for the previous 12 months was 4.0%. 4.3% - 4.0% = 0.3%, 20 basis points away from the beginning of a recession according to the Sahm calculation. This is certainly not the only measure of recession risk. But combining the rise in unemployment with student loan repayments possibly resuming and record high credit card delinquencies could be quite the millstone on consumer spending moving forward.

To Grow or Not to Grow

Lately we’ve been hearing from many clients that they’re slowing down loan growth as loan demand weakens in some markets and funding constraints make it difficult in most markets, all while the near-term economic outlook is foggy at best. However, we have heard from others that are either risk averse or moving forward with calibrated risk and still looking for growth opportunities where they can find them.

Even in the publicly traded market, there appear to be some banks that see this as an opportunity to seize market share. For example, Bank of Oklahoma (NASDAQGS: BOKF) recently mentioned in its 2023 Q3 earnings call that because of the bank’s strong capital position, BOKF wants to take advantage of the fact that other banks in their markets are retreating or pulling back.

For those banks that choose to seize growth opportunities in the current environment, it needs to be asked whether they’re securing an appropriate risk-adjusted return. If deposit pricing is stabilizing but macro conditions are becoming more volatile, all banks, growing and shrinking alike, need to seriously consider whether they’re receiving an appropriate return for the risk they’re taking this late in the economic cycle.

Our hunch is that many banks are forfeiting yield, and more importantly perhaps, loan fees, the attainment of which could serve as a margin of safety for their shareholders if these newly-booked credits sour.

It is incumbent upon lenders to help their customers understand that lending decisions at present require greater scrutiny. Lenders need to showcase the ability to manage expectations as this increased scrutiny will necessarily increase the time it takes to get loans funded. It’s important for bank management teams to also account for this increased cost of deliberation and careful underwriting when pricing these deals.

We don’t pretend to know what the coming new year will bring, but we do have some familiar canaries in the coal mine warning us of trouble. Banks would be wise to proceed with caution and to ensure they’re adequately compensated when they do choose to extend credit in today’s environment.